invoice finance4 min read

Invoice Finance: How Faster Quotes Transform Cash Flow for Growing BusinessesA guide to APIs, data standards, and the future of creditworthiness assessment

The UK SME lending market is undergoing a quiet revolution. Not through flashy fintech startups or blockchain hype, but through something more fundamental: open banking.

For decades, lenders have assessed SME creditworthiness using limited, outdated data. Bank statements. Tax returns. A handful of financial ratios. Alternative lenders have tried to work around this by relying on workarounds: merchant data, ad hoc API connections, self-reported figures that don’t reflect reality.

Open banking changes this fundamentally. For the first time, lenders can access verified financial data in real time, directly from accounting systems and banks. APIs have moved from niche integration to industry standard. Data standards have created a common language across platforms.

This is how creditworthiness assessment is being reinvented.

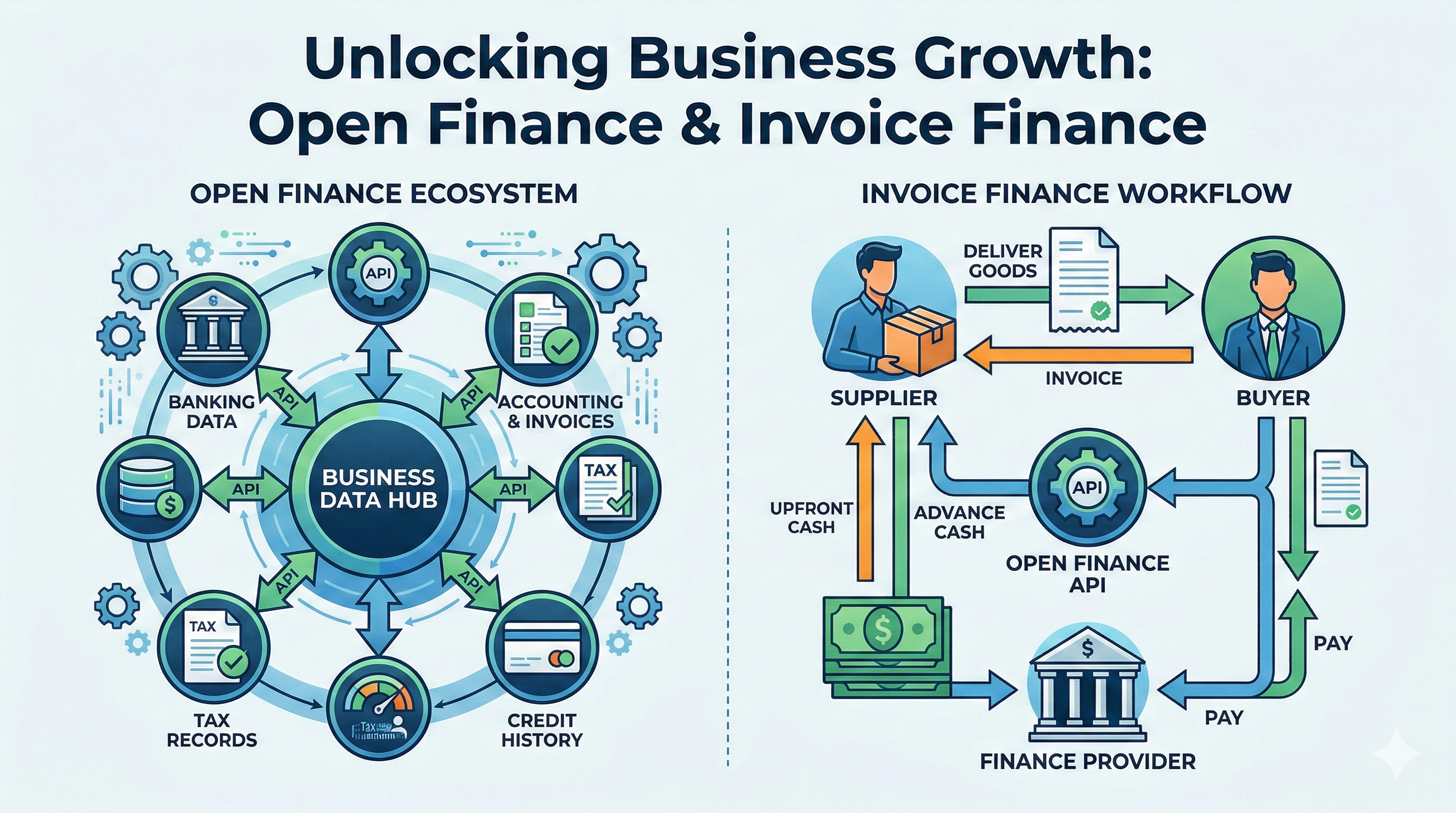

Open banking is a regulatory initiative that enables the secure sharing of customer financial data between different institutions. In the UK, the Open Banking Standard was introduced through PSD2 (Payment Services Directive 2) and continues to evolve through the FCA’s Open Finance roadmap.

Put simply: a customer can grant permission for a fintech platform, lender, or broker to access their financial data directly from their bank or accounting software. No manual downloads. No PDFs. No delay.

The impact has been profound. Over 750,000 SMEs in the UK now use open banking products for cash management, forecasting, and finance applications. The shift is accelerating.

For lending, this matters because creditworthiness assessment has always been hampered by data quality and currency. Open banking solves both problems at once.

An API (Application Programming Interface) is simply a standardised way for software systems to talk to each other. In SME lending, APIs allow lenders to pull data automatically from accounting systems like Xero and Sage, and from banking platforms.

This might seem technical, but the practical implications are enormous.

Traditional lending relied on audited accounts: historical snapshots, often 6-18 months old. By the time a lender saw the data, business conditions had likely changed significantly.

APIs enable real-time access to live P&L, balance sheet, and cash flow information. A lender can now assess the business as it exists today, not as it existed last year.

This transforms speed and accuracy in equal measure.

Brokers spend hours manually entering figures from accounts into application forms. Errors creep in. Data gets misaligned. Lenders then spend more hours verifying and cross-checking.

APIs eliminate this entirely. Financial data flows directly from the source system into the lender’s underwriting platform. No retyping. No transcription errors. No delays.

One of our broker partners recently told us that our integrated Xero pipeline saved them 12 hours per deal, purely on data entry and verification.

When data is sourced via API from verified systems, there’s an unbroken audit trail. Regulators can see exactly where figures came from. No disputes about whether a bank statement is ‘real.’

This compliance benefit has become increasingly valuable as lenders face tighter regulations around affordability and creditworthiness assessment.

APIs are only as useful as the data flowing through them. If Xero sends data in one format and Sage in another, and banks in a third, lenders face a chaos of interpretation.

This is why data standards matter enormously.

The UK has adopted the Open Banking Standard, which defines exactly how financial data should be structured, labelled, and transmitted. A merchant’s trading history looks the same whether it comes from Barclays or NatWest. A P&L statement has consistent line items across providers.

With standardised data, lenders can build algorithms that work across multiple providers. They can automate creditworthiness assessments. They can identify patterns and risk factors with confidence.

The alternative: proprietary data formats. Each integration becomes a one-off engineering effort. It’s expensive. It scales poorly. It’s essentially where we were before open banking.

| Data Element | Without Standards | With Standards |

|---|---|---|

| Transactions | Manual extraction, format varies by bank | Standardised transaction schema, API delivery |

| P&L | Custom formats, manual interpretation | Consistent line items, automated ingestion |

| Assertions & Metadata | Ambiguous, relies on context | Clear definitions, verifiable source |

Alternative lenders include specialist finance houses, peer-to-peer platforms, and invoice finance providers. All have always had to move faster than traditional banks. They’ve needed to make lending decisions with less data and in shorter timescales.

Open banking and APIs are giving them the tools to do this responsibly.

For invoice finance and working capital providers, the critical question is always: can this business service the debt? Open banking lets them see real-time cash in and cash out. They can assess liquidity trends without relying on forecasts or old bank statements.

This is a game-changer for businesses with volatile cash flows.

With standardised data from thousands of SMEs, lenders can now build robust benchmarks for different sectors. A cleaning contractor’s financial profile should look different from a software developer’s. Open banking data allows lenders to see and react to these differences with precision.

This shifts assessment from ‘rules-based’ to ‘evidence-based’, a subtle but powerful change.

When financial data is standardised and delivered via API, underwriting can be partly or fully automated. Many lenders are now building scorecards that run in seconds, with human underwriters focusing only on edge cases or high-value deals.

The result: lending decisions in days instead of weeks.

Brokers sit at the centre of this change. Open banking benefits them enormously, but only if they’re using platforms designed to leverage it.

A broker armed with open banking tools can now:

The alternative is being left behind, working with the same manual processes, the same inefficiencies, the same time investment that made broking exhausting a decade ago.

Open banking doesn’t just benefit lenders. It empowers brokers to compete more effectively and serve clients faster.

Open banking is transformative, but it’s not without challenges.

With sensitive financial data flowing between systems, security is paramount. UK open banking operates under strict PSD2 and GDPR frameworks, requiring strong authentication and explicit customer consent. This is correct, but it also means platforms must invest heavily in compliance infrastructure.

Brokers and lenders need to partner with platforms that take this seriously.

Standardised data is only as good as the data being entered into the source system. A business using Xero but entering transactions haphazardly will still produce poor data. Open banking solves the delivery problem, not the quality problem.

Lenders still need to apply judgement and ask good questions.

Not every business uses modern accounting software. Some SMEs still work with legacy systems or spreadsheets. Open banking reaches most of the market, but not all of it. Lenders need fallback processes for these cases.

The best platforms handle this gracefully, offering manual upload options without degrading the overall user experience.

Here’s the interesting part: open banking isn’t just a fintech trend. It’s policy. The FCA has made open finance a central plank of its agenda, with an explicit roadmap to expand open banking into SME lending, insurance, and investment services through 2030.

This means lenders investing in open banking infrastructure now are future-proofing their operations. The regulator is explicitly encouraging this direction. New lenders entering the market are expected to use modern data standards from day one.

Lenders and brokers who adopt open banking early aren’t just gaining competitive advantage. They’re aligning themselves with the direction of regulation itself.

The shift from manual, paper-based lending to API-driven, open banking-based assessment is already underway. It’s not a future vision; it’s happening now, and accelerating.

In five years, lenders that still rely on manual data entry and historical accounts will be at a severe disadvantage. Brokers that can’t access verified real-time data will struggle to compete. The question isn’t whether to adopt open banking: it’s when.

For alternative lenders, this is an opportunity to level the playing field with traditional banks. Banks have scale, but they move slowly. Alternative lenders who embrace open banking can move faster, make better decisions, and serve SMEs with real urgency.

For brokers, it’s a chance to unlock genuine efficiency and reclaim the time currently spent on admin, research, and verification. The brokers who thrive in the next decade will be those who use technology to enhance their expertise, not replace it.

At FundingSearch, we’ve built open banking into our DNA. Our Xero and Sage integrations pull verified financial data directly into our lender matching engine, eliminating hours of broker research and dramatically improving application quality. We’re not just riding the wave of open banking; we’re helping to define what responsible, broker-first platforms should look like.

If you’re a broker looking to embrace open banking, or a lender wanting to streamline creditworthiness assessment, the time to act is now.

Discover how FundingSearch’s open banking platform can transform your lending operation. Visit fundingsearch.com or contact Phillip Evans