open banking,5 min read

How Open Banking is Changing SME LendingAll Posts

How intelligent data integration accelerates SME funding decisions and reduces broker research time.

| SME Funding Challenge | Figure |

|---|---|

| UK SMEs seeking commercial finance annually | 500,000+ |

| Average broker research time per deal | c20 hours |

| Lender application rejection rate | 50% |

| Average SME funding decision timeline | 6 to 8 weeks |

| Typical deal requiring due diligence rework | 45% |

| Smart Data Impact | Figure |

|---|---|

| Research time reduction | 95% (20+ hours to minutes) |

| Application completion time saved | 80% (6-8 hours to minutes) |

| Broker approval rate improvement | 40% |

| Due diligence time reduction | 60% |

| Average funding decision acceleration | 4 to 6 weeks faster |

An SME requires £150,000 working capital funding.

The business is profitable. Cashflow is healthy. The balance sheet is sound.

Yet eight weeks pass before receiving a lending decision.

Why?

The delay isn't about creditworthiness; it's about data.

In the UK commercial finance market, the absence of smart data creates systemic friction. Brokers waste 20 to 40 hours per deal researching lenders manually. Lenders receive 50% of applications that fail their initial screening due to mismatched criteria. SMEs endure extended decision timescales that amplify the stress of securing funding.

The entire process operates on unverified, fragmented information.

Step 1: Client Data Collection.

Brokers request financial information from SME clients. The client sends a spreadsheet. Or a PDF. Or last year's accounts. The numbers are self-reported. The data is often incomplete.

Step 2: Manual Compilation.

Brokers manually compile information into multiple lender application forms. Each lender has different field requirements. Each form demands different data formats.

Step 3: Lender Due Diligence.

Lenders receive applications with inconsistent formats and missing documentation. They cannot verify the data. They request bank statements. They commission accountancy reviews. They conduct extensive due diligence.

Step 4: Rejection or Approval.

50% of applications fail initial lender screening. The SME must reapply. The broker must restart research. The timeline extends.

| Broker Time Breakdown (per Deal) | Figure |

|---|---|

| Lender research and identification | 8 to 12 hours |

| Application form completion | 6 to 8 hours |

| Document gathering and verification | 3 to 5 hours |

| Lender communication and follow-up | 2 to 4 hours |

| Total average deal time | 20 to 40 hours |

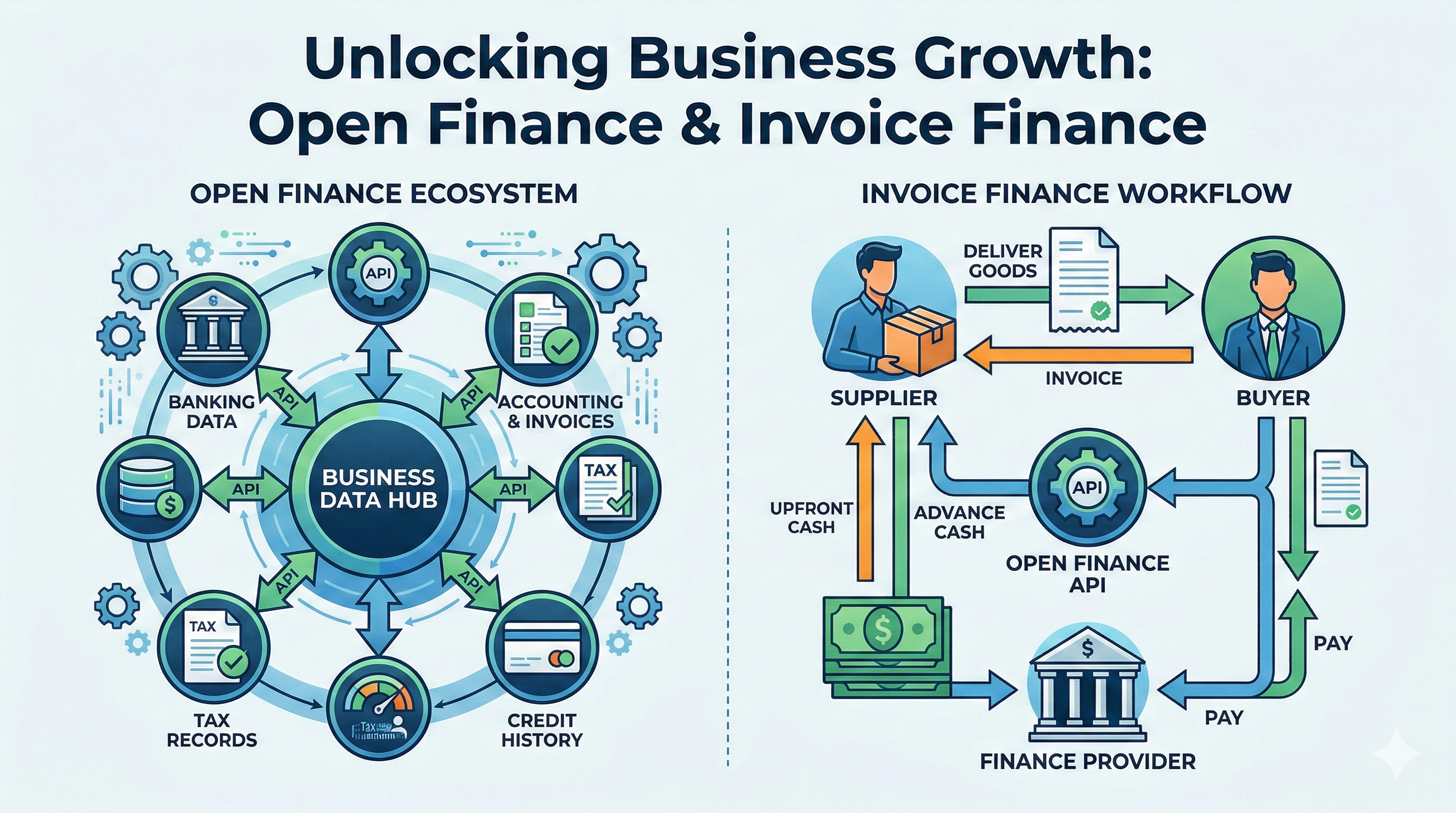

Smart data is verified, contextualised, and instantly accessible information.

In SME finance, smart data means:

Real-time financial information. Direct integration with Xero, Sage, and other accounting platforms means P&L, balance sheet, and cashflow data are pulled automatically. Data is never manually entered. Data is never self-reported. Data is always current.

Verified by trusted third parties. Data sourced from Companies House, HMRC, and accounting software carries inherent verification. It isn't a claim; it's a legal record.

Contextualised for decision making. The data isn't just historical numbers; it's analysed to provide insights into financial health, trading patterns, and lending risk.

Instantly shareable. The same verified dataset moves seamlessly between brokers, lenders, and SMEs. No retyping. No format conversion. No data loss.

Smart data eliminates friction at every stage.

For SMEs, smart data means faster access to capital. But it offers far more.

Reduced documentation burden. SMEs no longer gather spreadsheets, invoices, and statements. They provide their broker with access to their accounting software. The system does the rest. Documents are generated automatically.

Faster lending decisions. Lenders no longer require weeks to conduct due diligence. Verified, complete applications move through underwriting in days.

Better lender matching. Smart data allows platforms to match SMEs with lenders who actively want to fund businesses like theirs. No mismatched applications. No rejections based on poor fit.

Reduced costs. Many SMEs incur accountancy fees to prepare funding applications. Verified data from existing accounting software eliminates this need.

| SME Funding Timeline Comparison | Figure |

|---|---|

| Traditional process (weeks) | 6 to 8 |

| Smart data process (working days) | 10 to 15 |

| Time saved | 4 to 6 weeks |

| Stress reduction | Significant |

Commercial finance brokers face a productivity crisis.

The 20-hour research burden per deal is real. It's exhausting. It's unprofitable. It limits the number of clients a broker can serve.

Smart data transforms broker economics.

Intelligent lender matching. Instead of manually researching hundreds of lender criteria, brokers receive an instant ranked list of suitable lenders with match probability scores. Research time reduces from 20+ hours to minutes.

Automated application completion. A master application fed with verified data automatically populates individual lender forms. Form completion time reduces from 6 to 8 hours to minutes.

Higher approval rates. Lenders receive higher quality applications. Mismatches are eliminated. Approval rates improve by 40% on average.

Professional client experience. Brokers can offer SME clients a contemporary, streamlined experience that differentiates them from manual competitors.

| Broker Productivity Gains (per Deal) | Figure |

|---|---|

| Time saved on research and matching | 15 to 20 hours |

| Time saved on application completion | 5 to 6 hours |

| Total time saved per deal | 20 to 26 hours |

| Client capacity increase (same headcount) | 200% to 300% |

| Approval rate improvement | 40% average |

Commercial lenders face an application quality crisis.

They receive hundreds of applications monthly. Most are incomplete. Many contain unverified information. Decision-making is slow and resource-intensive.

Smart data solves this.

Pre-qualified applications. Applications arrive with verified financial data and intelligent pre-screening. They have already passed baseline criteria checks. Lenders receive applications they can approve.

Reduced due diligence. Complete, verified information means lenders no longer chase documentation for weeks. Due diligence time reduces by 60% on average.

Better credit decisions. Verified data enables faster, more accurate credit assessment. Risk is evaluated on complete information.

Improved volumes. Lenders can process more applications with same headcount. Operational costs reduce per application. Margins improve.

| Lender Operational Impact (per Application) | Figure |

|---|---|

| Due diligence time reduction | 60% |

| Application rejection rate improvement | 45% fewer mismatches |

| Time to credit decision | Days (vs weeks) |

| Underwriting team productivity | Up to 60% gain |

| Application processing cost reduction | Up to 50% |

The Financial Conduct Authority has made regulatory direction unambiguous.

The FCA's Vision 2030 explicitly envisions UK SME lending powered by verified financial data integration and open finance principles.

The FCA's SME Finance TechSprint brought together innovative fintech companies to demonstrate how open finance solves real SME lending challenges.

The message is unambiguous: UK SME finance is moving toward smart data.

For brokers and lenders, this has practical implications. Organisations adopting smart data solutions today build infrastructure defining competitive advantage tomorrow. Those that delay risk falling behind.

The UK commercial finance market is substantial.

| UK Commercial Finance Market Size | Figure |

|---|---|

| Annual commercial finance lending volume | £38+ billion |

| SMEs seeking commercial finance annually | 500,000+ |

| Commercial finance brokers (UK) | 2,000+ |

| Alternative finance providers | 500+ |

| Banks offering commercial finance | 60+ |

Yet the infrastructure remains rooted in 20th century processes.

Most lender decisions still rely on manual application review and document gathering.

This is the opportunity. Smart data solves a problem affecting hundreds of thousands of SMEs annually.

Smart data is no longer theoretical.

Platforms integrating verified financial data with intelligent matching are operational. Brokers are reducing deal research time from weeks to hours. Lenders are processing applications in days rather than weeks.

The transition is accelerating.

For SMEs seeking funding, smart data platforms offer relief. Faster decisions. Less documentation. Faster access to capital from lenders who want to fund them.

For brokers, smart data represents reclaimed capacity. Increased client volumes. Competitive differentiation.

For lenders, it means pre-qualified applications, reduced costs, and improved credit decisions.

This is why I built FundingSearch. After ten years as a commercial finance broker, I saw the same problems repeat endlessly. SMEs waiting. Brokers stressed. Lenders frustrated. And everyone working with incomplete, unverified information.

Smart data fixes this.

The technology exists. The regulatory direction is clear. Market demand is obvious. The question now is how quickly brokers and lenders transition to smarter working.